Hauptinhalt

Split pay is here to stay.Numbers prove it.

11,4%

installment spend

increase

2017-2022

Source: credi2

42%

of consumers want

card-led installments

Source: Visa

300%

CAGR to be

generated by

card-linked loans

Source: credi2

Top 6 benefits

- Add “micro instalments” to any charge or debit card

- Pre-, at-, post purchase payment feature

- Completely scheme agnostic

- Plug-and-play: Product UI, core banking, operation

- Unlocks untapped POS and e-com potential

- Fast time-to-market

Instalment on cardsdisrupt the credit landscape.

-

Consumers prefer card-linked BNPL: Broader economic trends have shaped consumer expectations, threatening traditional brand loyalty. In fact, 42% of consumers prefer card-linked instalments.

-

Time to market: Embedded finance helps to jump start digital and automated pay later products. Technology has enabled new players to enter the market and boosted credit decisioning capabilities.

-

Regulation favours banks: Regulatory change continues to encourage responsible lending. An upcoming EU Consumer Credit Directive will provide protection for instalments of up to € 200.

-

EURIBOR increase. The constant increase drives refinancing costs and affects commercial models. Banks benefit from lower internal refinancing and can offer more attractive pricings than fintechs can do.

Top use casesfor instalment on cards

Issuer based instalments use cases range from pre-purchase and real time to post-purchase.

-

Pre-purchase

Pre-purchase determined card-led instalments: "Pre-set" means that payments will automatically be splitted in certain number of instalments dependant on the issuer. Linked to certain amounts, merchant category codes or eg. time periods. This methods turn every debit or charge card into a trusted and easy to use BNPL product.

-

Real time

“At-purchase”: Consumers can split their purchases in their banking app in real time - similar to Apple Pay Later. This POS linked feature does not require any merchant integration nor sign up to a BNPL provider. Consumers can use their trusted and well known issuer / banking app to split payments their way.

-

Post-purchase

Post-purchase is the use case with the biggest untapped potential. Consumers can split their spendings a few days after purchasing directly in their issuer app. By picking a single eligible transaction and turning it into an instalment, debit and credit cards offer more convenience and an unmatched degree of payment flexibilty.

Card-led instalment productsFor credit or debit cards.

Credi2's BNPL platform offers three card-led options.

Easily embedded with maximum convenience.

-

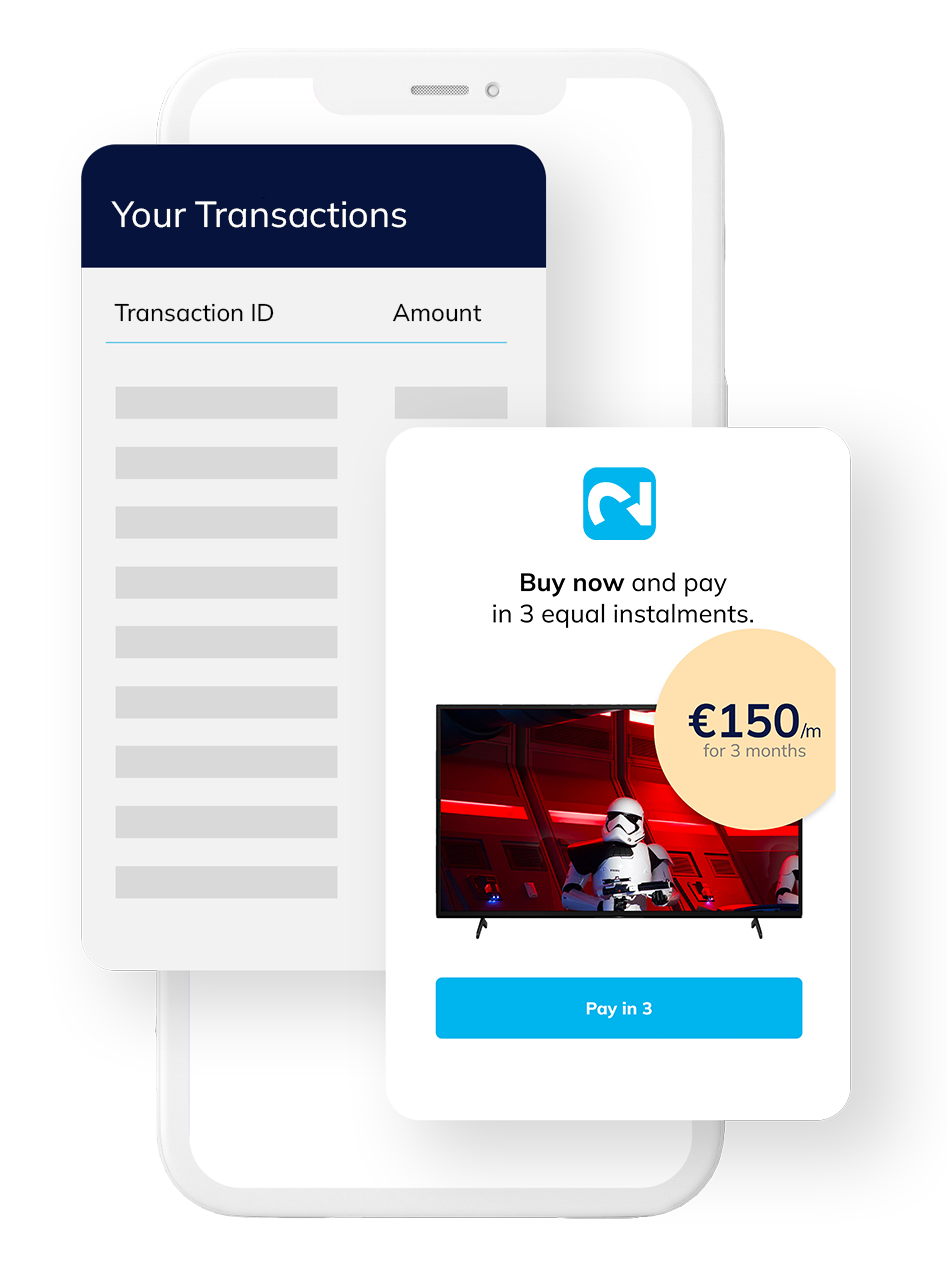

Pay in 3/6/9

“Pay in 3/6/9” is a flexible payment method where customers can choose between a credit or debit card payment and pay in predefined equal installments within a certain number of days.

-

Pay flex

“Pay Flex” is the most flexible payment method for consumer by choosing a custom instalment period or monthly repayment amount. Linked to charge- or debit cards this offers great payment convenience and new revenue streams for issuers. Making it an attractive option for those who prefer to spread out their payments over time with more flexibilty.

-

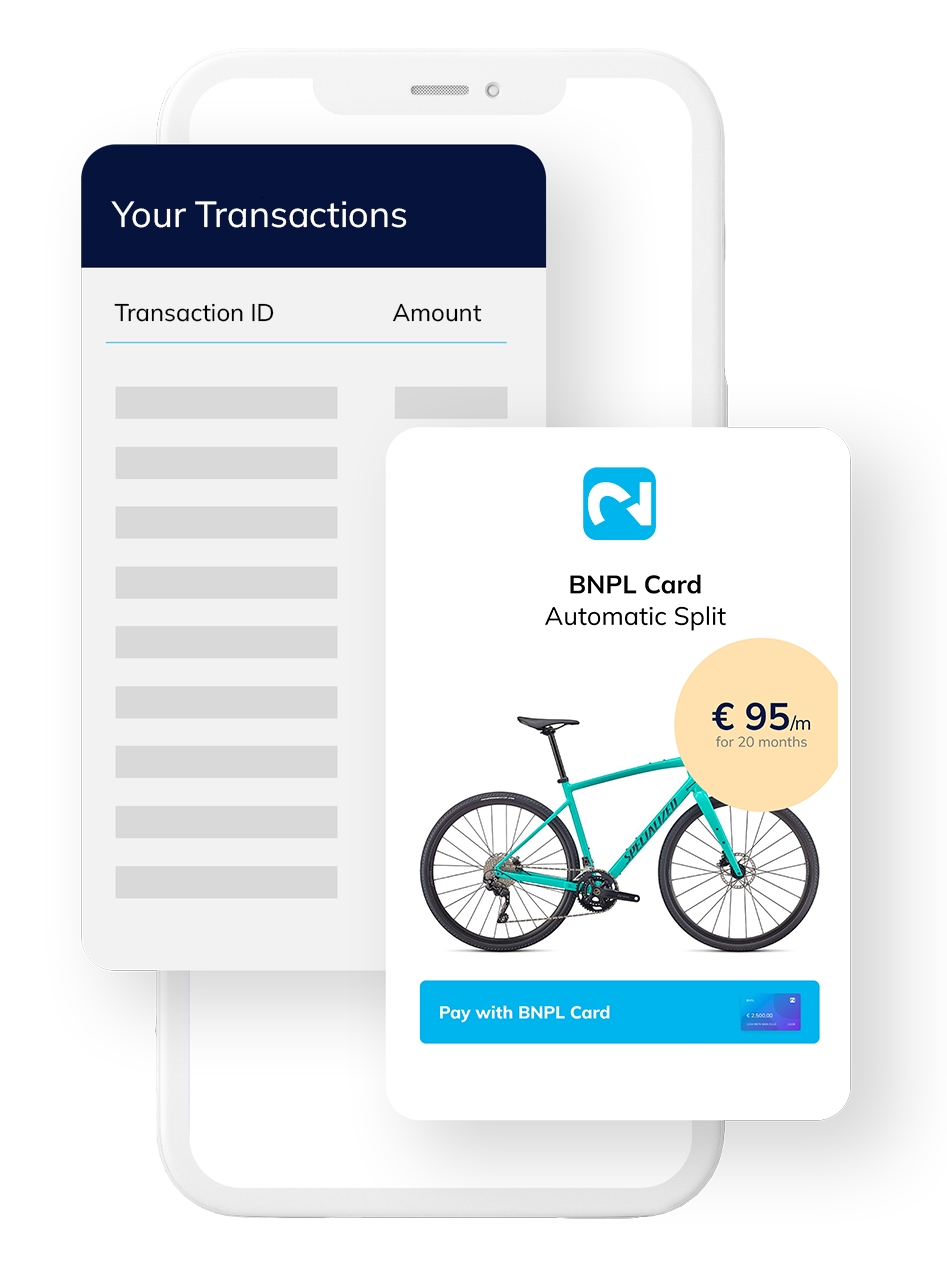

BNPL card

The virtual BNPL card is a digital version of a common credit card, used for online purchases and in-store transactions with a automatic preset split functionally. Consumers can easily split the cost of their purchase into instalments without any further action.

Credi2 Blog

Launching a card-led installment product: The challenges

Read more

Card-led pay later solutions are here to stay

Read more

We are ready to work together.

FAQs

Merchants leverage the following advantages:

1. Trust and relationship with existing partnering bank

2. Customer trust in established bank

3. Labeling BNPL service with merchant branding and deep intergration

4. Reduction of operational effort and costs at the merchant

5. Reown customer journey and data to optimize Customer life time value

The payout comes from the bank operating the BNPL solution.

In most cases credi2 operates the customer service on behalf of the bank for technical and consumer related support.

Yes. That's one of the core advantages of white label based BNPL solutions.