Hauptinhalt

Lending is here to stay.Numbers prove it.

$995 bln

Buy now, pay later

market size in 2026.

Source: Juniper Research

900 mil

BNPL users by 2027.

Source: Juniper Research

82%

of consumers appreciate the simple application process for BNPL.

Source: Credi2 study, 2021

Top 5 benefits

Banks and issuers set the digital financing standard with credi2's Embedding Lending-as-a-service platform for any instalment or BNPL product.

- Fast time to market

- Growth: reach Gen Y & Z

- Online. Mobile. Point of Sale

- White-label end-to-end solution

- Reduce implementation efforts and costs

The market favors lendersto take over.

-

Tighter EU regulation for BNPL & higher refinancing costs clearly favor banks and issuers to step into the Pay Later market and take over.

-

Generation Y & Z favor flexible buy now, pay later driving 274% growth, creating a $1 trillion opportunity by 2026.

-

42% of consumers want credit card linked BNPL.

Post-purchase installments to generate 200-300% CAGR.

Embedded Lendinguse cases

Embedded financing covers any pre-, during-, and post-purchase use cases along the customer journey. With any instalment or BNPL product.

-

eCommerce financing

Nowadays buy now, pay later financing methods are responsible for up to 70% of check-outs. Furthermore, they push revenues by up to 15-30% in many verticals by attracting new incremental target groups like Gen Y & Z. Offering popular split pay or payable by invoice payments based on your own white-labeled BNPL platform comes with more control, better commercial rates and ultimately more revenue. Banks and retail can leverage their unique advantages through credi2's pay later platform.

-

Point of Sale financing

Consumers expect a seamless omni-channel experience and therefore the same payment flexibility at the physical POS. With modern, easy to use, fast and 100% digital retail financing methods like installment loans, split pay or pay on invoice, consumers can be served with the same advantages known from eCommerce. Release store staff from complex processes, while benefitting from bigger shopping baskets and more revenue. Banks and Retail can unleash this untapped potential.

-

Instalment on cards

Issuers can easily enter the buy now, pay later market by leveraging their unique positioning and being the inventors of pay later payments decades ago. By offering pre- and post-purchase instalments, linked to a virtual BNPL charge card, any post-purchase credit card transaction can be converted into an installment solution. Offering consumers more flexibility and product convenience. Issuers can therefore build up a credit book to create new revenue streams and offer an alternative to embedded BNPL solution.

-

Cash loan

Offering a cash loan within 10-15min, under your brand, fully digital. That's what many financial players would do too. Serving consumers when they need smart liquity management. Credi2's fully digital platform deploys instalments loans under your banks brand, by liberating you from all IT, operation and product hassles, so you can focus on going to market.

What our customers say

-

"With the credi2 platform we further automated our lending business, saved costs and shortened our time-to-market."

Dr. Michael Reinhart

Chairman of the Mgmt Board -

“Thanks to the cooperation with credi2, we can reach even more customers with the Cyberport subscription model for Apple products.”

René Bittner

CEO procurement

Cyberport

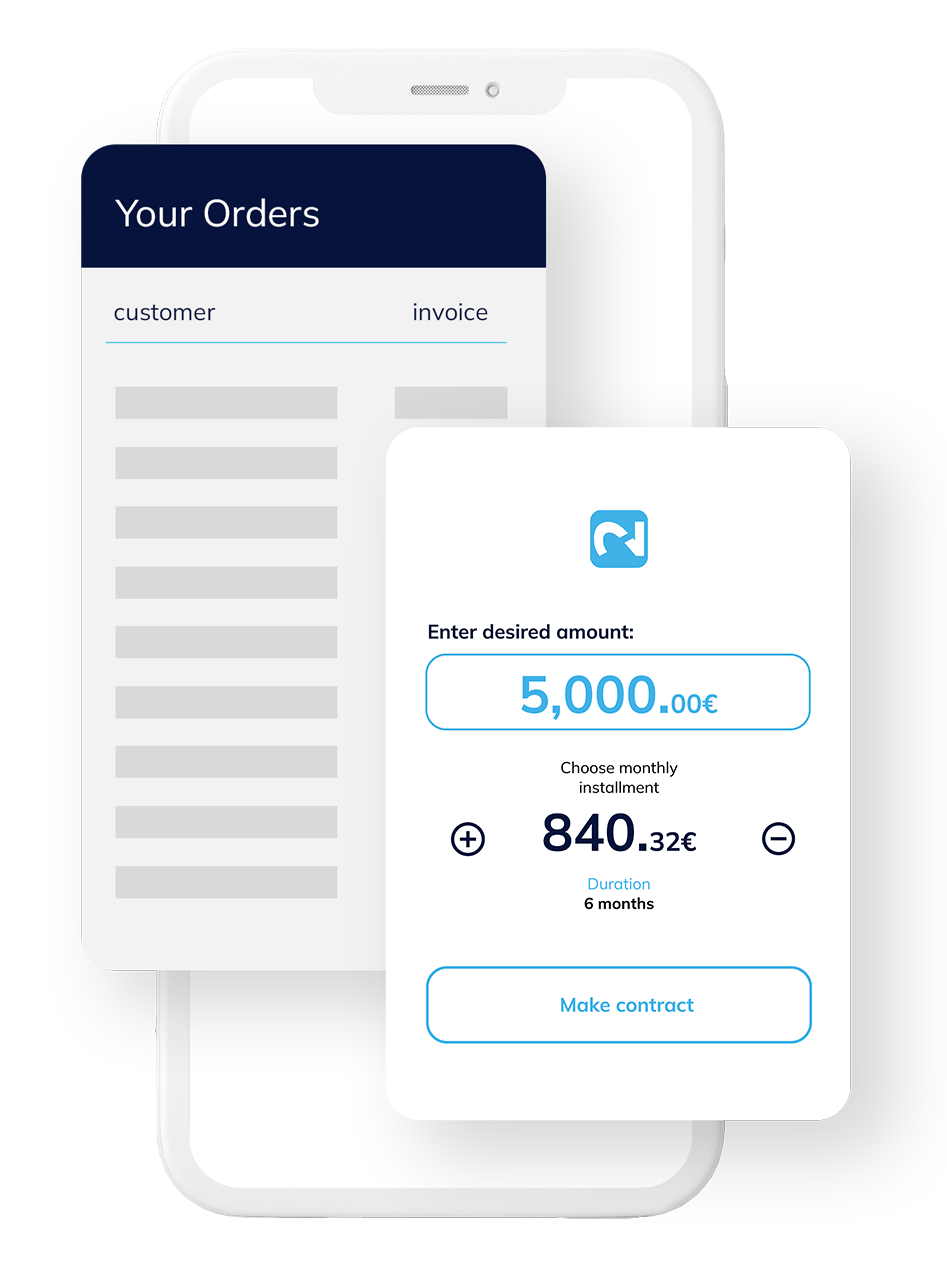

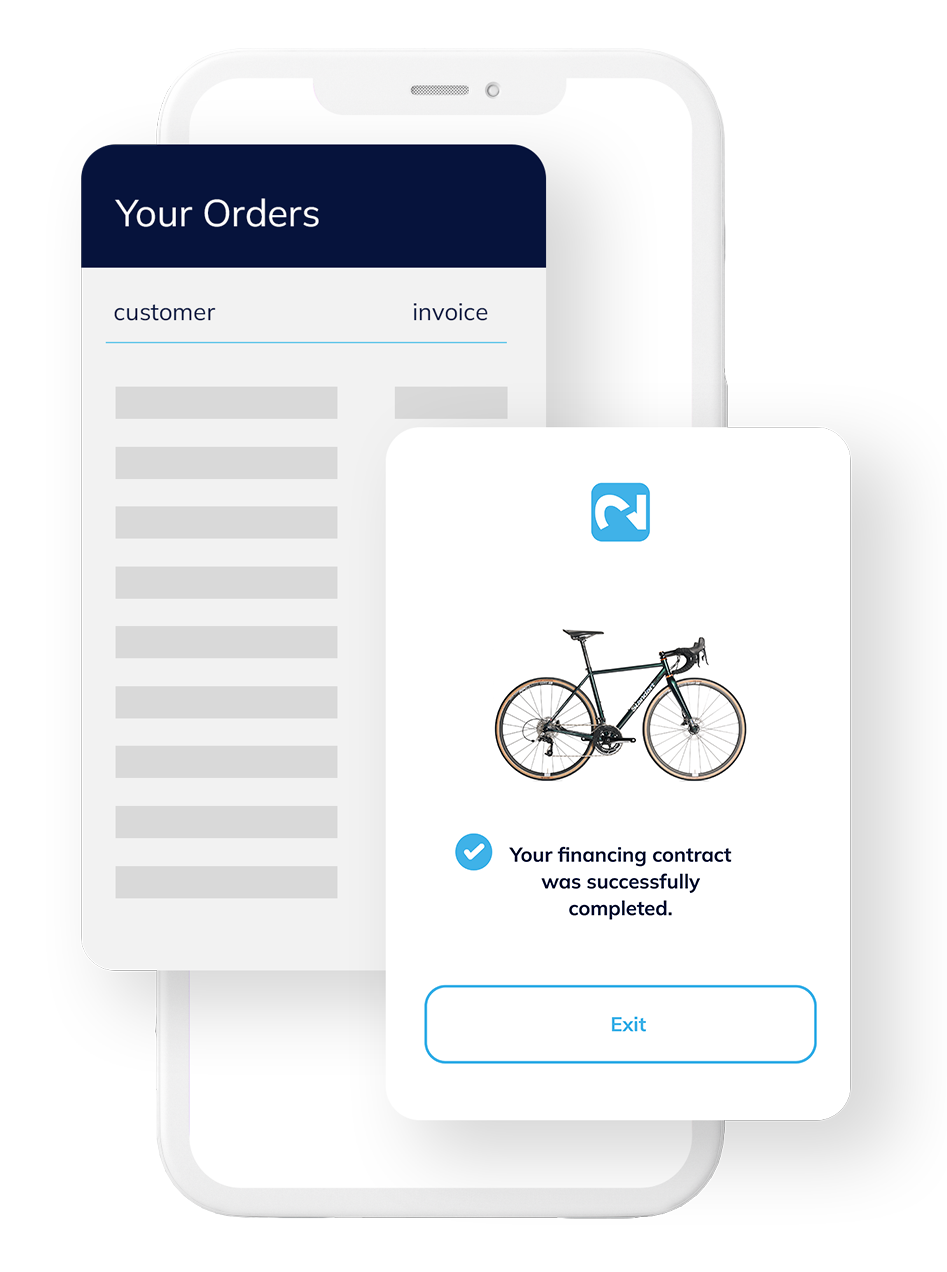

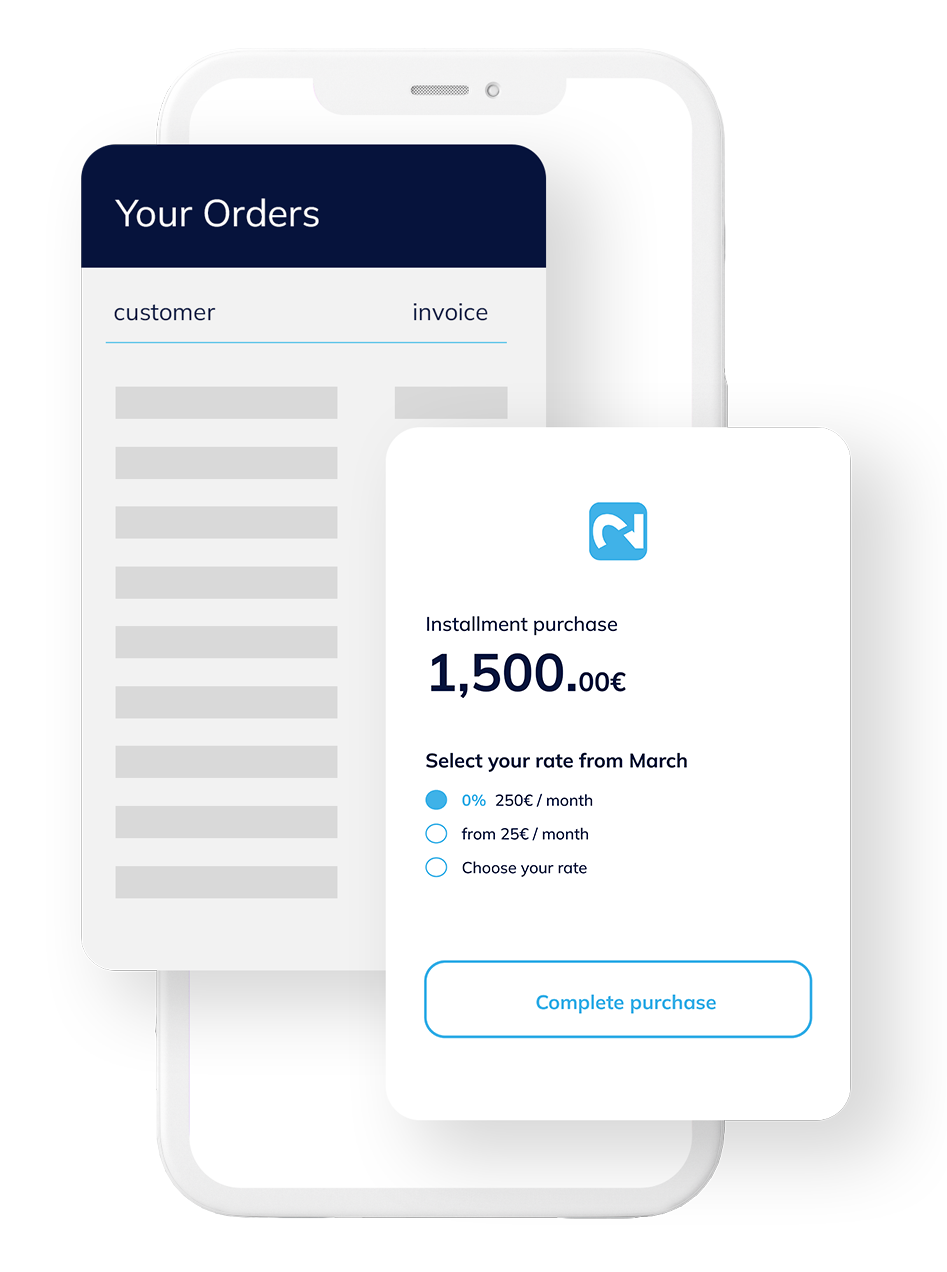

The best financing product for your business model.

Credi2's BNPL platform offers four flexible white-label financing products. Easily embedded at any payment touchpoint.

-

Pay per invoice

The eCommerce champion to drive conversions.

Consumers pay the purchase balance by invoice after a term of typically 14 days - interest free. This financing method provides payment flexiblity like chargecards do - but less complicated. And it works with the return management.

-

Split pay

The fastest installment payment in 3-5 min.

Split pay allows consumers to typcially pay later in 3-5 monthly installments. Depending on the credit score typcially up to €1,000. Split pay normaly comes with a light KYC process to drive eCommerce conversions.

-

Installment loan

A full flegged credit in 5-10 min.

Credit-based financing comes with full KYC for high value products or big baskets up to €20,000. Duration can be flexible adjusted and installments can go to 84 rates.

-

Revolving credit

The flexible credit line.

This credit-based product offers consumers maximum flexibility in terms of installment rates, credit duration and repayments options in combination with a fix credit line.

Latest news

Launching a card-led installment product: The challenges

Read more

Card-led pay later solutions are here to stay

Read more

Lets go into the details.Top FAQ's

The credi2 solutions offer a variety of risk- and onboarding models for customers. From a simple credit scoring including basic identification and fraud prevention mechanisms up to a fully AML-compliant customer onboarding including QES service can be provided. The provided models and processes comply with regulatory requirements to fit the products offered best.

The risk and onboarding solution of credi2 services are configured and setup based on your individual needs and specifications. All solutions can be adjusted to your needs ranging from incorporation your preferred partners to utilization of your existing models and services.

Customer and merchant portals can be provided and offer e.g. transaction and payment overviews, payment management and reporting and document management capabilites.

All services and solutions can be operated as white label services or as partner branded solutions.